Are property taxes on 1098

Your mortgage lender might pay your real estate taxes from an escrow account. If so, they’ll send you Form 1098. This form will report any real estate taxes you paid.

Where is the real estate tax on 1098?

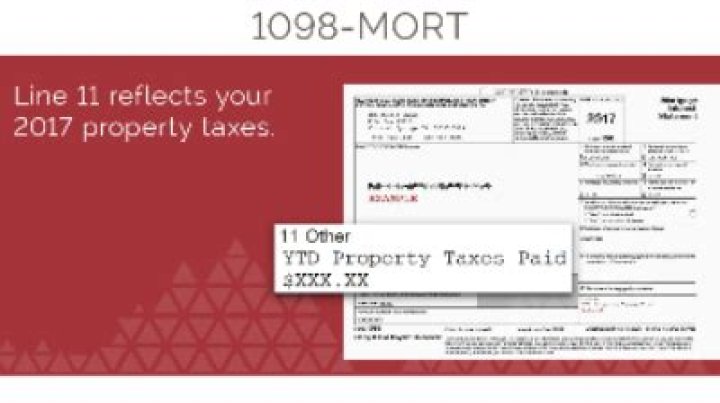

The amount of real estate taxes paid may be reported to you on Form 1098, Box 4 Mortgage Interest Statement.

How does 1098 mortgage affect taxes?

The amount shown as interest paid on Form 1098 is the amount you deduct on your tax return. Where do I take this deduction? … If you received Form 1098 reporting the amount of mortgage interest you paid for the year, record your interest deduction on Line 8a. If you didn’t receive Form 1098, use Line 8b instead.

Why doesn't my 1098 show any real estate taxes paid?

Your lender sends one copy to you and one to the Internal Revenue Service. If you take the mortgage interest write-off, the form gives you and the government a record of how much interest you paid. But, even if your lender handles your property tax payments, that information may not appear on your 1098.Is mortgage tax the same as property tax?

If you pay your mortgage, it’s likely you are already paying your California real property taxes.

Can you deduct property taxes if you don't itemize?

A: Unfortunately, this is not still allowed, and there is no way to deduct your property taxes on your federal income tax return without itemizing. Five years ago, Congress passed a bill allowing a single person to deduct up to $500 of property taxes on a primary residence in addition to their standard deduction.

Are property taxes deductible on federal taxes?

Homeowners who itemize their tax returns can deduct property taxes they pay on their main residence and any other real estate they own. This includes property taxes you pay starting from the date you purchase the property.

What is the 2021 standard deduction?

Filing StatusStandard Deduction 2021Standard Deduction 2022Single; Married Filing Separately$12,550$12,950Married Filing Jointly & Surviving Spouses$25,100$25,900Head of Household$18,800$19,400Can estate tax be deducted on Schedule A?

Some taxes and fees you can’t deduct on Schedule A include federal income taxes, social security taxes, transfer taxes (or stamp taxes) on the sale of property, homeowner’s association fees, estate and inheritance taxes, and service charges for water, sewer, or trash collection.

Are closing costs tax deductible 2020?If you itemize your taxes, you can usually deduct your closing costs in the year that you closed on your home. If you closed on your home in 2020, you can deduct these costs on your 2020 taxes. The amount you paid must be clearly shown and itemized on your loan’s closing disclosure or settlement statement.

Article first time published onHow does property tax deductible work?

Property Tax Deduction Property taxes are generally still tax-deductible, but this year the deduction is subject to a total cap of $10,000, which includes property taxes plus state and local income taxes or sales taxes paid during the year ($5,000 if married filing separately).

How do I report a home purchase on my taxes?

- You have a gain and do not qualify to exclude all of it,

- You have a gain and choose not to exclude it, or.

- You received a Form 1099-S.

Does a 1098 increase refund?

Your 1098-T may qualify you for education-related tax benefits like the American Opportunity Credit, Lifetime Learning Credit, or the Tuition and Fees Deduction. … If the credit amount exceeds the amount of tax you owe, you can receive up to $1,000 of the credit as a refund.

How can I avoid property taxes?

- Consider holding your property within a limited company. …

- Transfer property to your spouse. …

- Make the most of allowable expenses. …

- Increase your rent. …

- Change to an offset buy-to-let mortgage. …

- Before you do anything…

Is real estate and property tax the same thing?

Real estate taxes are the same as real property taxes. They are levied on most properties in America and paid to state and local governments. The funds generated from real estate taxes (or real property taxes) are typically used to help pay for local and state services.

Do you pay property taxes monthly?

Are Property Taxes Paid Monthly? Property taxes are not paid monthly. They’re usually paid biannually (twice a year) or annually. You pay this tax when you own a home or other real property in a state or location that charges it.

Are mortgages tax deductible?

Taxpayers can deduct the interest paid on first and second mortgages up to $1,000,000 in mortgage debt (the limit is $500,000 if married and filing separately). Any interest paid on first or second mortgages over this amount is not tax deductible. … The most common mortgage terms are 15 years and 30 years.

How much is property tax in the US?

California’s overall property taxes are below the national average. The average effective property tax rate in California is 0.73%, compared to the national rate, which sits at 1.07%.

What deductions can I claim if I don't itemize?

- Educator Expenses. …

- Student Loan Interest. …

- HSA Contributions. …

- IRA Contributions. …

- Self-Employed Retirement Contributions. …

- Early Withdrawal Penalties. …

- Alimony Payments. …

- Certain Business Expenses.

Is it better to take standard deduction or itemize?

Add up your itemized deductions and compare the total to the standard deduction available for your filing status. If your itemized deductions are greater than the standard deduction, then itemizing makes sense for you. If you’re below that threshold, then claiming the standard deduction makes more sense.

What itemized deductions are no longer available?

In addition, you can no longer claim “miscellaneous itemized deductions,” such as tax preparation fees, investment management fees, and unreimbursed employee expenses. In the past, you could deduct those to the extent the total miscellaneous itemized deductions exceeded 2 percent of your adjusted gross income.

What is the estate tax exemption in 2020?

The Tax Cuts and Jobs Act (TCJA) doubled the estate tax exemption to $11.18 million for singles and $22.36 million for married couples, but only for 2018 through 2025. The exemption level is indexed for inflation reaching $11.4 million in 2019 and $11.58 million in 2020 (and twice those amounts for married couples).

Does everyone have to file an estate tax return?

IRS Form 1041, U.S. Income Tax Return for Estates and Trusts, is required if the estate generates more than $600 in annual gross income. The decedent and their estate are separate taxable entities. … Most deductions and credits allowed to individuals are also allowed to estates and trusts.

What assets are subject to estate tax?

The federal estate tax is a tax on property (cash, real estate, stock, or other assets) transferred from deceased persons to their heirs.

How much of my Social Security is taxable in 2021?

For the 2021 tax year, single filers with a combined income of $25,000 to $34,000 must pay income taxes on up to 50% of their Social Security benefits. If your combined income was more than $34,000, you will pay taxes on up to 85% of your Social Security benefits.

Does Social Security benefits count as income?

Since 1935, the U.S. Social Security Administration has provided benefits to retired or disabled individuals and their family members. … While Social Security benefits are not counted as part of gross income, they are included in combined income, which the IRS uses to determine if benefits are taxable.

Is Social Security income taxable?

Some of you have to pay federal income taxes on your Social Security benefits. between $25,000 and $34,000, you may have to pay income tax on up to 50 percent of your benefits. … more than $34,000, up to 85 percent of your benefits may be taxable.

What can you write off when you buy a house?

- Mortgage interest. For most people, the biggest tax break from owning a home comes from deducting mortgage interest. …

- Points. …

- Real estate taxes. …

- Mortgage Insurance Premiums. …

- Penalty-free IRA payouts for first-time buyers. …

- Home improvements. …

- Energy credits. …

- Tax-free profit on sale.

What is deductible when you buy a house?

The only tax deductions on a home purchase you may qualify for is the prepaid mortgage interest (points). … Ex: appraisal fees, inspection fees, title fees, attorney fees, or property taxes. The funds you provided at or before closing, including any points the seller paid, were at least as much as the points charged.

Can you write off home improvements?

Home improvements on a personal residence are generally not tax deductible for federal income taxes. However, installing energy efficient equipment on your property may qualify you for a tax credit, and renovations to a home for medical purposes may qualify as a tax deductible medical expense.

How much real estate tax can you write off?

The Cap On The Property Tax Deduction You can now deduct a total of $10,000 in state and local property taxes if you’re single, a head of household or if you’re married and filing jointly, and $5,000 if you’re married and filing separately.