Does GAAP use LIFO or FIFO

One of the most basic differences is that GAAP permits the use of all three of the most common methods for inventory accountability—weighted-average cost method; first in, first out (FIFO); and last in, first out (LIFO)—while the IFRS forbids the use of the LIFO method.

Which costing method is allowed under GAAP?

The generally accepted accounting matching principle requires manufacturing and service businesses to include direct and overhead expenses in product and service costs and, when appropriate, in inventory valuations. This means absorption costing is the only GAAP-approved costing method.

Which of these inventory methods are acceptable under US GAAP?

Under GAAP, FIFO (first in first out), LIFO (last in first out), weighted average, and specific identification are all acceptable methods of cost determination for your company’s inventory.

What are 4 factors that must be considered for accurate inventory valuation?

- Specific Identification.

- First-In, First-Out (FIFO)

- Last-In, First-Out (LIFO)

- Weighted Average Cost.

Which of the following inventory methods is allowed for external accounting IFRS GAAP?

Both GAAP and IFRS allow First In, First Out (FIFO), weighted-average cost, and specific identification methods for valuing inventories. However, GAAP also allows the Last In, First Out (LIFO) method, which is not allowed under IFRS.

Does cost accounting follow GAAP?

Cost accounting, because it is used as an internal tool by management, does not have to meet any specific standard such as generally accepted accounting principles (GAAP) and, as a result, varies in use from company to company or department to department.

What is inventory GAAP?

The Inventory Management-GAAP Connection Put simply, it’s the amount of money that an item can be sold for in a given market. For example, GAAP states that all inventory reserves be stated and valued using either the cost or the market value method, whichever is lower.

Is GAAP standard cost inventory?

Financial reporting: Standard costing systems track both standard and actual costs in a manufacturer’s general ledger. … The actual costs are used to track actual spending, and periodically adjust the value of inventory from standard cost (which is not GAAP-compliant) to actual cost (which is GAAP-compliant).How do you value inventory under GAAP?

Under US GAAP, inventories are measured at the lower of cost, market value, or net realisable value depending upon the inventory method used. Market value is defined as current replacement cost subject to an upper limit of net realizable value and a lower limit of net realizable value less a normal profit margin.

What are the four methods of inventory valuation?The four main inventory valuation methods are FIFO or First-In, First-Out; LIFO or Last-In, First-Out; Specific Identification; and Weighted Average Cost.

Article first time published onWhat are the methods of inventory control?

- Economic order quantity. …

- Minimum order quantity. …

- ABC analysis. …

- Just-in-time inventory management. …

- Safety stock inventory. …

- FIFO and LIFO. …

- Reorder point formula. …

- Batch tracking.

Why are inventory valuation methods important?

The way a company values its inventory directly affects its cost of goods sold (COGS), gross income and the monetary value of inventory remaining at the end of each period. Therefore, inventory valuation affects the profitability of a company and its potential value, as presented in its financial statements.

What's included in the cost of goods sold?

Cost of goods sold is the total amount your business paid as a cost directly related to the sale of products. Depending on your business, that may include products purchased for resale, raw materials, packaging, and direct labor related to producing or selling the good.

Which inventory costing method uses the newest cost for cost of goods sold?

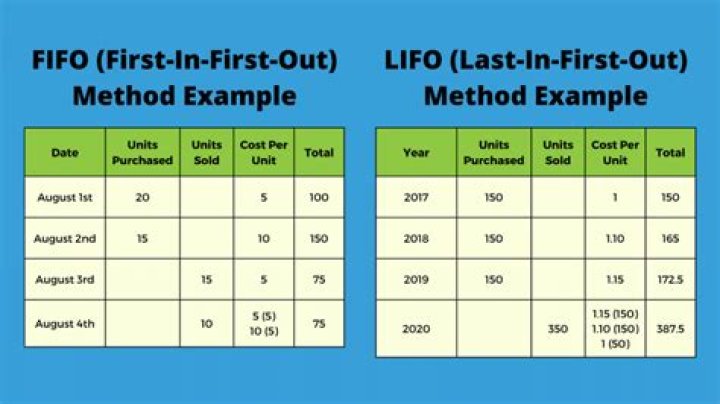

Last In, First Out (LIFO) Method Last in, first out (LIFO) is another inventory costing method a company can use to value the cost of goods sold. This method is the opposite of FIFO. Instead of selling its oldest inventory first, companies that use the LIFO method sell its newest inventory first.

Which inventory costing method uses the oldest cost for cost of goods sold?

FIFO (First in, First out) – this means you will use the OLDEST inventory first to fill orders. This also means the oldest costs will appear in Cost of Goods Sold (since this is an Expense account this also means oldest costs will appear in the Income Statement).

What is the average cost method for inventory?

The average cost method assigns a cost to inventory items based on the total cost of goods purchased or produced in a period divided by the total number of items purchased or produced. The average cost method is also known as the weighted-average method.

What comprises the cost of inventory?

The cost of inventory includes the cost of purchased merchandise, less discounts that are taken, plus any duties and transportation costs paid by the purchaser. … Technically, inventory costs include warehousing and insurance expenses associated with storing unsold merchandise.

Which costing method is used for external reporting?

Under generally accepted accounting principles (GAAP), absorption costing is required for external reporting. Absorption costing is an accounting method that captures all of the costs involved in manufacturing a product when valuing inventory.

Why are companies required by GAAP to measure inventories at the lower of cost or net realizable value?

Obsolescence, over supply, defects, major price declines, and similar problems can contribute to uncertainty about the “realization” (conversion to cash) for inventory items. Therefore, accountants evaluate inventory and employ lower of cost or net realizable value considerations.

Is GAAP a standard cost?

Standard costing will meet the GAAP requirements if the variances between the standard costs and the actual costs are properly prorated to the inventories and to the cost of goods sold prior to issuing the financial statements. …

How do you find GAAP rules?

The Financial Accounting Standards Board (FASB) provides free online access to the Accounting Standards Codification and is the only authoritative source for US GAAP.

What are the 4 types of cost?

Direct, indirect, fixed, and variable are the 4 main kinds of cost.

What are costing methods?

Costing Method – The way that a final product’s total cost is calculated. … Standard Cost – Manufacturers add up the costs of all the parts in a bill of materials, labor costs, and other costs incurred in the manufacturing process to come up with a final cost for each final product.

Is GAAP a variable cost?

Variable costing is not accepted by GAAP because it reports a lower taxable figure as inventory increases. In the eyes of the Internal Revenue Service, lower taxable income means less tax revenue.

What is FIFO method of inventory valuation?

First In, First Out, commonly known as FIFO, is an asset-management and valuation method in which assets produced or acquired first are sold, used, or disposed of first. For tax purposes, FIFO assumes that assets with the oldest costs are included in the income statement’s cost of goods sold (COGS).

What is GAAP accounting rules?

Generally Accepted Accounting Principles (GAAP or US GAAP) are a collection of commonly-followed accounting rules and standards for financial reporting. … The purpose of GAAP is to ensure that financial reporting is transparent and consistent from one organization to another.

How does GAAP perspective affect the inventory management?

GAAP calls for reporting inventory reserves by the lower of either the cost method or the market value method. … Inventory reserves offset the balance of inventory accounts. GAAP requires that inventory is stated at replacement cost if there is a difference between the market value and the replacement value.

How many cost accounting standards are there?

The Cost Accounting Standards (CAS) consist of nineteen standards promulgated by the Cost Accounting Standards Board (CASB) designed to ensure uniformity and consistency in the measurement, assignment, and allocation of costs to contracts with the United States Government.

What are the 5 methods of valuation?

- Asset Valuation. Your company’s assets include tangible and intangible items. …

- Historical Earnings Valuation. …

- Relative Valuation. …

- Future Maintainable Earnings Valuation. …

- Discount Cash Flow Valuation.

What is the first step in measuring inventory and cost of goods sold?

When calculating COGS, the first step is to determine the beginning cost of inventory and the ending cost of inventory for your reporting period. Here’s an example.

Which one of the following methods is allowed under GAAP but not under IFRS?

Which one of the following methods is allowed under GAAP but not under IFRS? LIFO is allowed under GAAP, but prohibited under IFRS.