How do you find out how many firms are in a market

divide the the aggregate demand at the equilibrium price by the output of each firm to get the number of firms.

How do you determine how many firms are in a market?

Given the market quantity, and the individual firm’s quantity produced we can calculate the number of firms: nq*=Q* Total output is Q*=10 000 and each firm produces q*=50 units, so there must be n=10 000 / 50=200 firms.

What are firms in a market?

A firm is a commercial enterprise, a company that buys and sells products and/or services to consumers with the aim of making a profit. In the world of commerce, the term is usually synonymous with ‘company’, or ‘business’ as in “She runs a forex trading business.”

How do you find the number of firms in the short run?

Set demand equal to supply and find 100-4Q=Q, so Q=20, P=20. b) How many firms are in the industry in the short run? Perfectly competitive firms will set P=MC, so 20=4+4q, so q=4. If each perfectly competitive firm is producing 4, market output is 20, there will be 5 perfectly competitive firms in the industry.How many firms are there?

Based on data from the U.S. Census Bureau, there were 6.1 million employer firms in the United States in 2018 (latest data):

How do you calculate short run output?

Calculate average variable cost (AVC) by dividing TVC by output (Q) of units produced. For example, if during the short run you produced 450 widgets, the AVC is $1.67 if Q is 450 (750/ 450). Add your AFC and AVC to obtain short run total costs (TC). From the previous example, total average costs equal $4.45.

How many firms are in monopolistic competition?

Market PowerNumber of FirmsPerfect CompetitionNoneInfiniteMonopolistic CompetitionLowManyMonopolyHighOne

How do you determine if a firm will produce in the short run?

- Increase production if the marginal cost is less than the marginal revenue.

- Decrease production if marginal cost is greater than marginal revenue.

- Continue producing if average variable cost is less than price per unit.

How do you find the short run equilibrium quantity?

- The short run supply function for each firm is. …

- Thus the aggregate supply (given that there are 50 firms) is. …

- The aggregate demand is Qd(p) = 1900 5p.

- The equilibrium price satisfies the equation 25p 500 = 1900 5p if the solution of this equation is at least 20. …

- The output of each firm is (1/2)(80) 10 = 30.

Production units will be called as firms.

Article first time published onHow many types of firms are there?

Typically, there are four main types of businesses: Sole ProprietorshipsSole ProprietorshipA sole proprietorship (also known as individual entrepreneurship, sole trader, or proprietorship) is a type of an unincorporated entity that is owned only, Partnerships, Limited Liability Companies (LLC)Limited Liability Company …

What is an example of a firm?

The definition of firm is solid, hard or rigid. An example of firm is a sturdy piece of wood. … A firm is defined as a business with two or more persons. An example of firm is a law office.

What does the number of firms mean?

relationship between the number of firms in the market and market size. The general idea is that if competition is increasing in the number of. firms then the minimum per firm market size, denoted by the per firm. entry threshold, has to be increasing for firms to cover fixed cost.

How many firms are there in a perfectly competitive market?

Key Takeaways: In a monopolistic market, there is only one firm that dictates the price and supply levels of goods and services. A perfectly competitive market is composed of many firms, where no one firm has market control. In the real world, no market is purely monopolistic or perfectly competitive.

How many businesses are small businesses?

There are 30.2 million small businesses in the United States, according to the Small Business Administration’s (SBA) Office of Advocacy. Small businesses comprise 99.9 percent of all U.S. businesses.

How many firms are in an oligopoly?

A monopoly is a market with only one producer, a duopoly has two firms, and an oligopoly consists of two or more firms.

When an industry has many firms the industry is?

Monopolistic competition characterizes an industry in which many firms offer products or services that are similar (but not perfect) substitutes. Barriers to entry and exit in a monopolistic competitive industry are low, and the decisions of any one firm do not directly affect those of its competitors.

What are the 4 types of market structures?

Economic market structures can be grouped into four categories: perfect competition, monopolistic competition, oligopoly, and monopoly.

How do you calculate long run output?

- Take the derivative of average total cost. …

- Set the derivative equal to zero and solve for q. …

- Determine the long-run price.

How do you find the long run supply function?

The long‐run market supply curve is found by examining the responsiveness of short‐run market supply to a change in market demand. Consider the market demand and supply curves depicted in Figures (a) and (b).

How do I calculate marginal product?

The formula for calculating marginal product is (Q^n – Q^n-1) / (L^n – L^n-1).

What does P times Q mean?

From Wikipedia, the free encyclopedia. Total revenue is the total receipts a seller can obtain from selling goods or services to buyers. It can be written as P × Q, which is the price of the goods multiplied by the quantity of the sold goods.

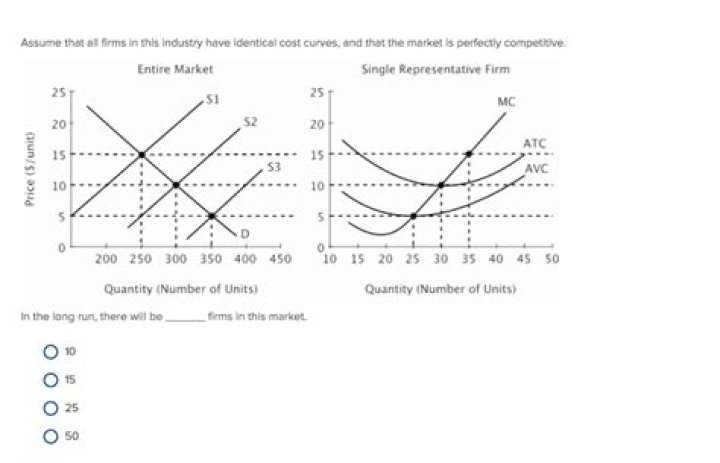

How many firms are in the market in the long run equilibrium?

Thus the long run equilibrium output of each firm is 100. The minimum of LAC is LAC(100) = (100)2 20,000 + 10,100 = 100. Thus the long run equilibrium price is 100. The aggregate demand at the price 100 is Qd(100) = 3000, so there are 3000/100 = 30 firms.

What is the short run market quantity?

Summary. Short-run supply is defined as the current supply given a firm’s capital expenditure on fixed assets – such as property, plant, and equipment. The break-even price is equal to the minimum average total cost.

What is short run market?

The short run is a concept that states that, within a certain period in the future, at least one input is fixed while others are variable. In economics, it expresses the idea that an economy behaves differently depending on the length of time it has to react to certain stimuli.

How do you determine if a firm should shut down?

Looking at Table 8.6, if the price falls below $2.05, the minimum average variable cost, the firm must shut down. The intersection of the average variable cost curve and the marginal cost curve, which shows the price where the firm would lack enough revenue to cover its variable costs, is called the shutdown point.

When a firm minimizes its losses in the short run?

In the short run, losses will be minimized as long as the firm covers its variable costs. In the long run, all costs are variable. Thus, all costs must be covered if the firm is to remain in business. 2.

How the prices of a perfectly competitive firm are determined in a short run?

Short-run price is determined by short-run equilibrium between demand and supply. Supply curve in the short run under perfect competition is a lateral summation of the short-run marginal cost curves of the firm.

Is a firm a business?

A firm is a for-profit business, usually formed as a partnership that provides professional services, such as legal or accounting services. … Not to be confused with a firm, a company is a business that sells goods and/or services for profit and includes all business structures and trades.

What is the difference between business and firm?

A firm refers to a business involved in the selling of services and products for profit, usually professional services. On the other hand, a company refers to a business involved in any income-generating activity involving the sale of goods and services and includes all business trades and structures.

Is a bank a firm?

A bank, as normally used, is a local office or branch of a company. The term bank does not mean a company per se. The Bank of England, for example, may well be a company, but it is not a bank in the ordinary sense of the word.