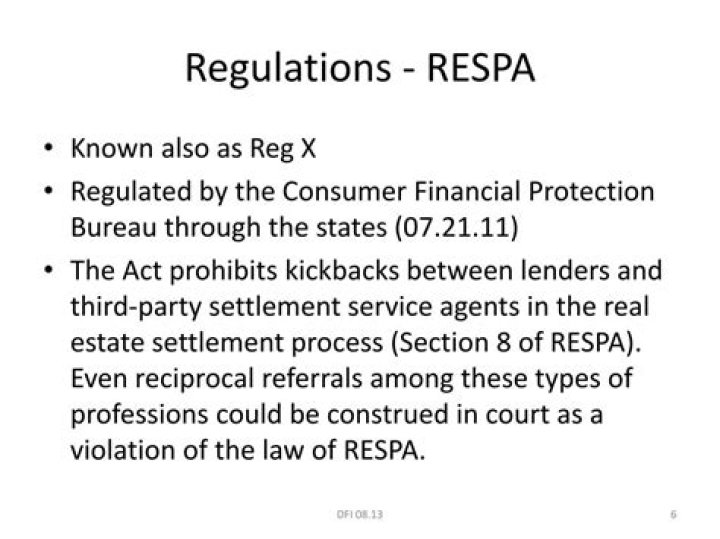

What does RESPA regulates

RESPA applies to the majority of purchase loans, refinances, property improvement loans, and equity lines of credit. … RESPA prohibits loan servicers from demanding excessively large escrow accounts and restricts sellers from mandating title insurance companies.

What is prohibited under RESPA?

Section 8 of RESPA prohibits anyone from giving or accepting a fee, kickback or anything of value in exchange for referrals of settlement service business involving a federally related mortgage loan. In addition, RESPA prohibits fee splitting and receiving unearned fees for services not actually performed.

What are the RESPA disclosures?

RESPA requires that borrowers receive disclosures at various times in the transaction process. Some disclosures spell out the costs associated with the settlement, outline lender servicing and escrow account practices and describe business relationships between settlement service providers.

Who must comply with RESPA?

RESPA covers any creditor that makes or invests in residential real estate loans aggregating more than $1,000,000 per year. of goods or services. Dealer loans are covered by RESPA if the obligations are to be assigned before the first payment is due to any lender or creditor otherwise subject to the regulation.What are the six items need to make a loan application for Trid disclosures?

The six items are the consumer’s name, income and social security number (to obtain a credit report), the property’s address, an estimate of property’s value and the loan amount sought.

What is considered a RESPA violation?

A RESPA violation occurs when a title company has a financial interest (or ownership) in a real estate transaction where a buyer’s loan is “federally insured.” RESPA is a consumer protection law created to make sure that buyers of residential properties of one to four family units are informed in detailed writing …

What are two things RESPA prohibits?

RESPA Section 8(a) and Regulation X, 12 CFR § 1024.14(b), prohibit giving or accepting a fee, kickback, or thing of value pursuant to an agreement or understanding (oral or otherwise), for referrals of business incident to or part of a settlement service involving a federally related mortgage loan.

Does RESPA apply to HELOCs?

The TILA-RESPA rule applies to most closed-end consumer credit transactions secured by real property, but does not apply to: HELOCs; • Reverse mortgages; or • Chattel-dwelling loans, such as loans secured by a mobile home or by a dwelling that is not attached to real property (i.e., land).What is a qualified written request?

A Qualified Written Request, or QWR, is written correspondence that you or someone acting on your behalf can send to your mortgage servicer. … You can send a QWR to request information about the servicing of your mortgage loan or to assert that the company has made an error.

Does RESPA Section 8 apply to HELOCs?RESPA uses “federally related mortgage loan” for purposes of section 8 violations. … RESPA certainly does apply to HELOC’s but each disclosure is exempted.

Article first time published onWhat does Section 8 of RESPA prohibit?

RESPA Section 8(a) prohibits the giving and accepting of kickbacks (e.g., cash or other “things of value” as defined in RESPA and Regulation X) pursuant to any agreement or understanding to refer settlement service business or business incident to a real estate settlement service in connection with those loans.

What disclosures are required for a mortgage loan?

Loan Application When you apply for a mortgage, the lender or the mortgage broker must give you several disclosures, including a good faith estimate, a mortgage servicing disclosure statement, and a consumer information booklet. The good faith estimate spells out the estimated fees you’ll need to pay at closing.

What are Trid requirements?

TRID guidelines are designed to help borrowers understand the terms costs associated with of their loan more clearly before closing. TRID regulations govern the mortgage process and dictate what information lenders are required to provide to borrowers – as well as when they are required to provide it.

What are the 6 pieces of information for a mortgage application?

An application is defined as the submission of six pieces of information: (1) the consumer’s name, (2) the consumer’s income, (3) the consumer’s Social Security number to obtain a credit report (or other unique identifier if the consumer has no Social Security number), (4) the property address, (5) an estimate of the …

What are the 6 elements of Trid?

- Name.

- Income.

- Social Security Number.

- Property Address.

- Estimated Value of Property.

- Mortgage Loan Amount sought.

Which disclosures are required by respa for Trid loans at origination?

When you’re looking for a mortgage, TRID guidelines dictate that your mortgage lender must provide you with two unique disclosures: the Loan Estimate and the Closing Disclosure.

What is the 3 7 3 rule in mortgage terms?

The 3/7/3 Rule requires a seven business day waiting period once the initial disclosure is provided before closing a home loan (business days are everyday except Sundays and Holidays).

How many elements are required to be considered a violation under Section 8 RESPA?

To violate the RESPA Section 8(a) prohibition against fees, kickbacks, or things of value and the equivalent Regulation X, Section 3500.14, three elements must be present. First, there must be a payment or giving of a thing of value. Second, the payment must be paramount to an agreement to refer business.

What are considered settlement services under RESPA?

A settlement service includes any service provided in connection with a real estate settlement including, but not limited to, title searches, title examinations, the provision of title certificates, title insurance, services rendered by an attorney, the preparation of documents, property surveys, the rendering of …

What loans are exempt from RESPA?

When a loan is made to purchase vacant land, and none of the proceeds of the loan will be used to construct a covered residential structure, the loan is exempt from RESPA oversight. This is another case of the relative experience and knowledge of the participants in the transaction.

What is the typical time required to maintain escrow records?

Which party holds the escrow money when a dispute occurs? What is the typical time period required to maintain escrow records? Which of the following classes are not protected by federal law? If a group of brokers have a meeting to set commission rates, what does this violate?

What is a respa letter?

A section of RESPA, 12 U.S.C. § 2605, provides a procedure and a remedy to obtain information from a loan servicer that fails to provide it under a more informal request. This form is an example of a “qualified written request” that meets the requirements of the law.

Can a written request be emailed?

Clearly, if email “written notice” is expressly allowed or prohibited, determining the answer is easy – follow the contract. Often, though, the contract is silent as to the form and substance of the written notice to be provided.

How long do construction loans usually last?

Because construction loans generally are intended to cover the building process, they’re typically issued for a period of 12 to 18 months. That said, some loans automatically convert into a permanent mortgage once construction is complete.

Does RESPA apply to condos?

Loans secured by a condominium unit or a cooperative share are covered under RESPA as long as the units are not used for business purposes. … Such a sale is exempt from RESPA coverage as a secondary market transaction.”

Does RESPA apply to private lenders?

While a private lender or broker who makes or arranges a federally-related loan is subject to RESPA requirements, neither a carryback seller nor the broker who arranges a carryback sale are subject to RESPA requirements.

Does RESPA apply to mobile homes?

The regulations do provide RESPA protections to certain owners of manufactured homes, as they apply to loans secured by real property upon which there is a manufactured home.

Is RESPA still in effect?

RESPA was signed into law in December 1974, and became effective on June 20, 1975. The law has gone through a number of changes and amendments since then, all with the intent of informing consumers of their settlement costs and prohibiting kickbacks that can increase the cost of obtaining a mortgage.

Is Reg Z the same as Tila?

The Truth in Lending Act (TILA) is implemented by the Board’s Regulation Z (12 CFR Part 226). A principal purpose of TILA is to promote the informed use of consumer credit by requiring disclosures about its terms and cost. TILA also includes substantive protections.

Are mobile home loans subject to RESPA?

The loan is not subject to RESPA; therefore, an initial escrow statement is not required. However, if the Bank is establishing an escrow account (i.e., loan is an HPML loan) then it is a best practice to provide an initial escrow disclosure.

Which required RESPA disclosures must be provided within three days of receipt of a loan application for a purchase?

RESPA requires mortgage brokers and lenders to provide borrowers with three specific disclosures at this point in the transaction: A Special Information Booklet must be provided to the prospective borrower at the time of the loan application or within three days thereafter.