What is a 721 c partnership

An IRC 721(c) partnership is any partnership to which a U.S. Transferor contributes IRC. 721(c) property if after the contribution and related transactions: 1. A related foreign person is a direct or indirect partner, AND. 2.

What is Section 721 property?

The IRS code section 721 allows an investor to transfer property held in a like-kind exchange for shares in a Real Estate Investment Trust (REIT) without triggering the need to pay for capital gains taxes. … Then, John can easily transfer the new property to a REIT in exchange for shares in the REIT.

WHAT IS 721c property?

Section 721(c) property is property, other than excluded property, with built-in gain that is contributed to a partnership by a U.S. transferor, including pursuant to a contribution described in § 1.721(c)-2(d) (partnership look-through rule).

What is a 721 transaction?

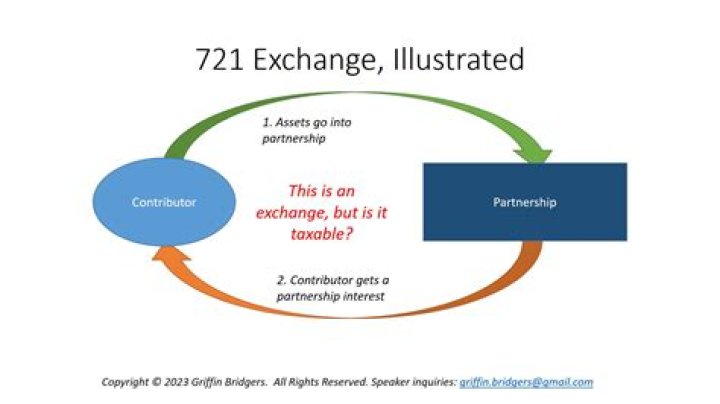

What is a 721 UPREIT Exchange? A 721 exchange is similar to the 1031 exchange. IRC Section 721 allows investors to exchange appreciated real estate property held for business or investment purposes for units in an operating partnership that will be converted into shares of the real estate investment trust (REIT).What is a Form 721c?

On January 18, 2017, the IRS issued temporary and proposed regulations (T.D. 9814) under Section 721(c) to address transfers of appreciated property by U.S. persons to partnerships with related foreign partners. … The regulations incorporate a number of taxpayer-friendly updates in response to comments on the Notice.

How do you qualify for a 1031 exchange?

To receive the full benefit of a 1031 exchange, your replacement property should be of equal or greater value. You must identify a replacement property for the assets sold within 45 days and then conclude the exchange within 180 days.

What is a 721 Upreit?

Section 721 of the Internal Revenue Code allows a property owner to contribute their property to a real estate investment trust (REIT) in exchange for an interest in the REIT. The process is sometimes referred to as a 721 UPREIT or UPREIT transaction.

How does a DST work?

DST is a seasonal time change measure where clocks are set ahead of standard time during part of the year. As DST starts, the Sun rises and sets later, on the clock, than the day before. Today, about 40% of countries worldwide have DST to make better use of daylight and conserve energy.Is cash a 721 property?

721(c) property generally includes any property that has built-in gain at the time it is contributed to the partnership, other than (1) a cash equivalent; (2) a “security” within the meaning of Sec.

What is a DST in real estate?A DST is an investment trust which holds one or more pieces of real property in which investors can purchase ownership interest in, thereby allowing investors to have a fractional ownership interest in the property held by that trust.

Article first time published onWhat is IRC section 267A?

IRC Section 267A generally disallows a deduction for interest or royalties paid or accrued in certain transactions involving a hybrid arrangement when US law allows a deduction, but the payee does not have a corresponding income inclusion under foreign tax law (deduction/no-inclusion (D/NI)).

What is IRS Section 6221 B?

Section 6221(b) (as amended by BBA) provides that certain partnerships with 100 or fewer partners may elect out of the centralized partnership audit regime. This schedule was created to allow partnerships to elect out of the centralized partnership audit regime.

What is designation of partnership representative?

The partnership can designate any person, entity, or itself as the representative, so long as they have a substantial presence in the United States. If an entity is designated, an individual who has a substantial presence in the U.S. must also be named to act on the entity’s behalf.

What is the centralized audit regime?

The centralized partnership audit regime, also referred to as BBA or PBBA, is generally effective for tax years beginning January 2018. … Under the BBA, the IRS generally assesses and collects any understatement of tax (called an imputed underpayment or IU) at the partnership level.

Is the partnership electing out of the centralized?

Partnerships with 100 or fewer partners for the taxable year can elect out of the centralized partnership audit regime if all partners are eligible partners.

What is the difference between a REIT and Upreit?

REITs are an entity that allows investors to make investment contributions for equity units or shares of the business. … The UPREIT is one such structure, primarily known for its allowance of property contributions in exchange for share ownership.

What is Upreit structure?

The term UPREIT (short for “Umbrella Partnership Real Estate Investment Trust”) refers to an entity structure that has been used by REIT’s since 1992 to allow selling property owners the ability to convert their ownership of one or more of their specific real estate properties into an interest which is‚ immediately‚ or …

What is Upreit and DownREIT?

An UpREIT allows investors to contribute their real estate investment holdings to an umbrella partnership in exchange for limited partnership units. A DownREIT allows investors to become partners in a partnership agreement with a REIT.

How long must you hold 1031 property?

If a property has been acquired through a 1031 Exchange and is later converted into a primary residence, it is necessary to hold the property for no less than five years or the sale will be fully taxable.

Can I buy a primary residence with a 1031 exchange?

A 1031 exchange generally only involves investment properties. Your primary residence isn’t typically eligible for a 1031 exchange. Even a second home that you live in some of the time is ineligible if you don’t treat it as an investment property for tax purposes.

Is it worth doing a 1031 exchange?

A 1031 Exchange allows you to delay paying your taxes. It doesn’t eliminate your capital gains tax. Only if you never sell your 1031 exchanged property or keep on doing a 1031 exchange, will you never incur a tax liability.

What is the basis of property inherited from a decedent?

The basis of property inherited from a decedent is generally one of the following: The fair market value (FMV) of the property on the date of the decedent’s death (whether or not the executor of the estate files an estate tax return (Form 706, United States Estate (and Generation-Skipping Transfer) Tax Return)).

What happens when a disregarded entity becomes a partnership?

A disregarded entity may sell an interest in that business and become a partnership. This conversion of a single member entity into a multiple member entity resulting from the issuance to the new member of an interest in the entity is considered Section 721 contributions to the entity by both partners.

What is a disguised sale?

A disguised sale transaction occurs when a partnership transfers money or other property to a partner that, in substance, is more properly characterized as a sale of property rather than a partnership distribution.

How does a DST make money?

No need to stress – DST offerings are essentially signed, sealed and delivered. Recurring monthly income potential. DST investments typically aim to make monthly distributions to investors. Due to its passive and recurring nature, some investors affectionately refer to this as “mailbox money”.

Who can invest in a DST?

Who can invest in a DST? You must be an “accredited investor” — an individual with a net worth in excess of $1 million, not including his or her home, OR an individual with income of over $200,000 per year over the last two years. If married, the combined income required is $300,000.

Why is DST used?

The main purpose of Daylight Saving Time (called “Summer Time” in many places in the world) is to make better use of daylight. We change our clocks during the summer months to move an hour of daylight from the morning to the evening. … According to some sources, DST saves energy.

How does a DST 1031 work?

A DST 1031 exchange property with a 50% loan to cost is a property wherein the investors are putting down 50% of the required equity or cash amount to purchase the 1031 exchange DST property and the lender is providing the other 50%, in the form of a loan.

Who pays DST?

The tax is paid by the person making, signing, issuing, accepting or transferring the documents. However, whenever one party to the taxable document enjoys exemption from the tax, the other party thereto who is not exempt shall be the one directly liable for the tax.

Are DST good investments?

DSTs can offer many retirement, tax and estate planning options. Passive income, elimination of personal liability, freedom, ability to manage cash flows and wealth transfer are just a few of the opportunities that DSTs can afford investors and their retirement planners.

What is Section 267 interest expense?

Section 267(a) requires that deductions for losses or unpaid expenses or interest described therein be disallowed even though the transaction in which such losses, expenses, or interest were incurred was a bona fide transaction.