What is a key rate duration

Key rate duration measures how the value of a debt security or a debt instrument portfolio, generally bonds, changes at a specific maturity point along the entirety of the yield curve.

What is a key rate?

The key rate is the interest rate at which banks can borrow when they fall short of their required reserves. They may borrow from other banks or directly from the Federal Reserve for a very short period of time.

How is key rate calculated?

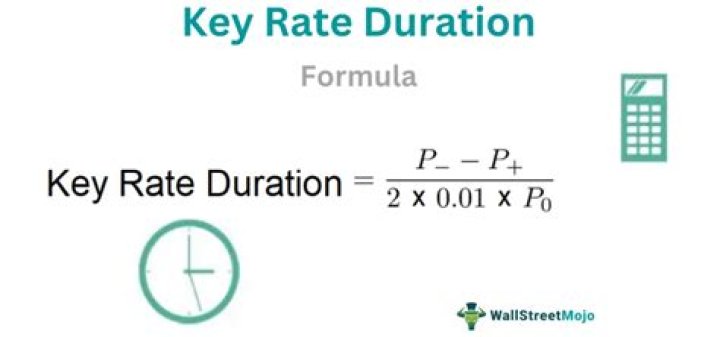

Formula for Calculating the Key Rate Duration P+ – /the bond’s price after a 1% increase in yield. P0 – The original price of the bond.

What is key rate duration CFA?

The key rate duration presents an improvement to the effective duration because it gives the expected changes in price when the yield curve shifts in a manner that is not perfectly parallel. … In other words, it measures a security’s sensitivity to shifts at “key” points along the yield curve.What is key rate exposure?

Key rate exposures help to describe the risk distribution along the term structure given a bond portfolio. … Partial ’01s are used to measure and hedge the risk of portfolios of swaps or portfolios that combine both bonds and swaps in terms of the most liquid money market and swap instruments.

Is Macaulay duration same as effective duration?

Effective Duration Effective duration is a measure of the duration for bonds with embedded options (e.g., callable bonds). Unlike the modified duration and Macaulay duration, effective duration considers fluctuations in the bond’s price movements relative to the changes in the bond’s yield to maturity (YTM).

What is key interest rate Canada?

The Bank of Canada leaves key policy rate at 0.25%, maintains forward guidance. The Bank of Canada kept the overnight rate at 0.25% and states it is continuing its reinvestment phase by keeping its holdings of Government of Canada bond roughly constant.

What does negative key rate duration mean?

For example, a 6-year zero-coupon bond will have a slightly higher price (because the 6-year spot rate is lower) when the 5-year key rate is increased; in other words, a 6-year zero-coupon bond will have a negative 5-year key rate duration. … When the price increases with a rate increase, duration must be negative.)Is Macaulay duration longer than maturity?

With all the other factors constant, a bond with a longer term to maturity assumes a greater Macaulay duration, as it takes a longer period to receive the principal payment at the maturity. It also means that Macaulay duration decreases as time passes (term to maturity shrinks).

What is the meaning of Macaulay duration?The Macaulay duration is the weighted average term to maturity of the cash flows from a bond. The weight of each cash flow is determined by dividing the present value of the cash flow by the price. Macaulay duration is frequently used by portfolio managers who use an immunization strategy.

Article first time published onWhat is the Sherman ratio?

The Sherman ratio is an interest rate risk measure and represents the yield per unit of duration. In other words, a Sherman ratio of 1 means that it would take a 100bps rise in interest rates over one year to offset the yield of a bond.

How do you calculate duration?

The formula for the duration is a measure of a bond’s sensitivity to changes in the interest rate, and it is calculated by dividing the sum product of discounted future cash inflow of the bond and a corresponding number of years by a sum of the discounted future cash inflow.

How does bond duration work?

Bond duration is a way of measuring how much bond prices are likely to change if and when interest rates move. In more technical terms, bond duration is measurement of interest rate risk. Understanding bond duration can help investors determine how bonds fit in to a broader investment portfolio.

How is Macaulay duration calculated?

The Macaulay duration is calculated by multiplying the time period by the periodic coupon payment and dividing the resulting value by 1 plus the periodic yield raised to the time to maturity.

What is DTS duration times spread?

Duration Times Spread (DTS) is the market standard method for measuring the credit volatility of a corporate bond. It is calculated by simply multiplying two readily available bond characteristics: the spread-durations and the credit spread.

What is the difference between duration and convexity?

Duration and convexity are two tools used to manage the risk exposure of fixed-income investments. Duration measures the bond’s sensitivity to interest rate changes. Convexity relates to the interaction between a bond’s price and its yield as it experiences changes in interest rates.

What's the meaning of partial duration?

A technique for applying some of the principles of duration analysis to rate changes that affect only part of the yield curve, typically the shorter end of the curve. Partial durations will sum to a value that is usually close to the overall effective duration.

Will interest rates go up in 2021?

Based on how low interest rates were in 2020, Mohtashami believes we’ll see the average mortgage interest rate inch upward in 2021. But it is difficult to see it going above 4% since we’re still in the thick of the COVID-19 pandemic, he says.

Will interest rates rise in 2021?

Interest rates are on the rise. And home prices have climbed at a record pace in 2021.

Can you lock in a variable rate mortgage?

Typically, the variable rate is lower than fixed, but can also float higher for periods. If you break the mortgage, the penalty is typically far lower. You can lock the variable rate into a fixed rate at any time, without breaking the mortgage.

What is effective duration vs modified duration?

While Effective Duration is a more complete measure of a bond’s sensitivity to interest rate movements versus the Macauley or Modified Duration measures, it still falls short because it is a linear approximation for small changes in yield; that is, it assumes that duration stays the same along the yield curve.

Can duration be greater than maturity?

The duration of any bond that pays a coupon will be less than its maturity, because some amount of coupon payments will be received before the maturity date. … The higher a bond’s coupon, the shorter its duration, because proportionately more payment is received before final maturity.

What is a good bond duration?

“A good rule of thumb is that for every 1 percent increase in bond yields, a 10-year duration bond will fall by approximately 10 percent,” Johnson says. … On the other hand, a bond with a duration of 30 years would fall 30 percent in value if bond yields rose by 1 percent.

What is Macaulay duration in debt fund?

Macaulay Duration is a measure of how long it takes for the price of a bond to be repaid by its internal cash flows. Macaulay Duration is used only for an instrument with fixed cash flows. Modified Duration as the name suggests, is a modified version of the Macaulay model that accounts for changing interest rates.

What is bond duration vs maturity?

In plain English, “duration” means “length of time” while “maturity” denotes “the extent to which something is full grown.” When bond investors talk about duration it has a very specific meaning: The sensitivity of a bond’s price to changes in interest rates.

What is duration example?

Duration is defined as the length of time that something lasts. When a film lasts for two hours, this is an example of a time when the film has a two hour duration. A measurement of a bond’s price sensitivity to changes in interest rates.

What does effective duration measure?

Effective duration calculates the expected price decline of a bond when interest rates rise by 1%. The value of the effective duration will always be lower than the maturity of the bond.

Why is modified duration better than maturity?

Modified duration is a slightly more involved calculation that takes into account the effects of interest-rate movements. Effective duration is another, still-more complicated measure used to assess interest-rate sensitivity when callable securities (those that may be paid off before maturity) are involved.

How do you calculate portfolio duration?

Portfolio duration is commonly estimated as the market-value-weighted average of the yield durations of the individual bonds in the portfolio. The total market value of the bond portfolio is 170,000 + 850,000 + 180,000 = 1,200,000.

What is one sided up duration?

The effective duration measure for a putable bond is 4.81. So any “up” movements in yield curves will be associated with smaller decreases in putable bond prices than the average, leading to the one-sided up duration being necessarily less than 4.81. …

What is a maturity matched rate?

If an option-free bond is trading at par, the bond’s maturity- matched rate (or the spot rate applicable to its maturity) is the only rate that affects the bond’s value. Its maturity key rate duration is the same as its effective duration, and all other key rate durations are zero.