What is IASB and its role

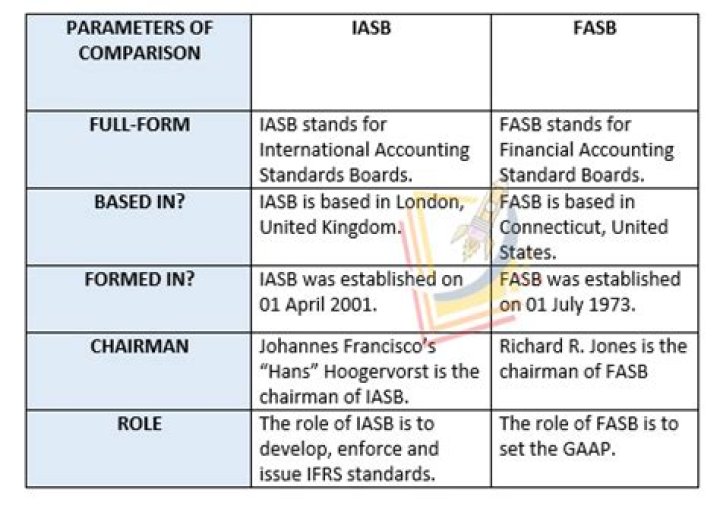

The International Accounting Standards Board (IASB) is an independent, private-sector body that develops and approves International Financial Reporting Standards (IFRSs). The IASB operates under the oversight of the IFRS Foundation.

What is IASB conceptual framework for financial reporting?

The Conceptual Framework states that only items that meet the definition of an asset, a liability or equity are recognised in the statement of financial position and only items that meet the definition of income or expenses are to be recognised in the statement(s) of financial performance.

What basis is used by the IASB in developing accounting principles and practices?

The framework states that “the measurement basis most commonly adopted by entities in preparing their financial statements is historical cost“. This however is often used with other bases, for example in IAS 2 ‘Inventories’, ‘the lower of cost and net realisable value”.

What are the accounting standards issued by the IASB?

What is IFRS? The International Financial Reporting Standards (IFRS) are accounting standards that are issued by the International Accounting Standards Board (IASB) with the objective of providing a common accounting language to increase transparency in the presentation of financial information.Why is the IASB conceptual framework important for accounting standards?

The primary purpose of the Conceptual Framework was to assist the IASB in the development of future IFRSs and in its review of existing IFRSs. The Conceptual Framework may also assist preparers of financial statements in developing accounting policies for transactions or events not covered by existing standards.

How does the IASB use the conceptual framework in developing IFRSs?

First, while the IASB used the Framework concepts to justify new lease accounting requirements, it also used an outside-the-Framework notion to justify a requirement. Second, accommodating constituents’ demands, it introduced rules in IFRS 16 to mitigate their concerns relating to high implementation costs.

What is the IASB framework for preparation and presentation of financial statements?

The Framework sets out the: (a) objective of financial reports; (b) assumptions underlying financial reports; (c) qualitative characteristics of financial reports; (d) elements of financial reports; and (e) recognition criteria for the elements of financial statements.

How does the IASB set standards?

Our standard-setting entails: public Board meetings broadcast live from our London office;agenda papers that inform the Board’s deliberations; discussion and decision summaries that are made available after meetings; and.Why is international accounting important?

Globally comparable accounting standards promote transparency, accountability, and efficiency in financial markets around the world. This enables investors and other market participants to make informed economic decisions about investment opportunities and risks and improves capital allocation.

What are the objectives of international financial reporting standards?The following are the objectives of IFRS: To establish a universal language for the companies to prepare the accounting statements. To establish accounting rules to make it easier for the stakeholders to interpret the financial statements, irrespective of the business location.

Article first time published onWhat are the main benefits of international harmonization of auditing standards?

The three main advantages of a single set of international accounting standards are (1) an increased comparability between firms, which reduces investor risk and facilitates cross-border financing and investment; (2) a reduction in the cost of preparing consolidated financial statements for multinational firms; and (3) …

Why does the IASB believe that a principles based approach to standard setting is superior to a rules based perspective?

Why does the IASB believe that a principles based approach to standard setting is superior to a rules based approach? … Principles based standard setting is less costly to undertake than rule based standard formulation.

Why is Conceptual Framework necessary in financial accounting?

The main reasons for developing an agreed conceptual framework are that it provides a framework for setting accounting standards, a basis for resolving accounting disputes, fundamental principles which then do not have to be repeated in accounting standards.

Which one of the following is the main aim of accounting?

The purpose of accounting is to accumulate and report on financial information about the performance, financial position, and cash flows of a business. This information is then used to reach decisions about how to manage the business, or invest in it, or lend money to it.

What are the qualitative characteristics of accounting information as identified in the IASB Conceptual Framework?

Relevance and faithful representation remain as the two fundamental qualitative characteristics. The four enhancing qualitative characteristics continue to be timeliness, understandability, verifiability and comparability.

How are financial statements related to the objective of financial reporting?

Objectives of financial statements are the specific purposes or reasons (which may include purpose of compliance, understanding the fundamentals of the company, measuring the financial strength of the business, reporting of the performance, results, financial stability and liquidity to the various stakeholders of the …

Who are general purpose financial statements primarily prepared for?

General-Purpose financial statements are prepared primarily for external users. They provide financial reporting information to a wide variety of users — shareholders, creditors, suppliers, employees, and regulators.

How do you prepare financial reports?

- Close the revenue accounts. Prepare one journal entry that debits all the revenue accounts. …

- Close the expense accounts. Prepare one journal entry that credits all the expense accounts. …

- Transfer the income summary balance to a capital account. …

- Close the drawing account.

Why did IASB revised conceptual framework?

Why have we revised the Conceptual Framework? In revising the Conceptual Framework, the Board sought a balance between providing high-level concepts and providing enough detail for the Conceptual Framework to be useful to the Board and others.

What are the purposes of the revised conceptual framework?

The revised conceptual framework introduces new concepts on measurement, presentation and disclosure, derecognition and has updated the definition of assets and liability, and derecognition criteria for assets and liabilities in financial statements.

How does conceptual framework contribute to the mission of IFRS?

(b) the Conceptual Framework contributes to the stated mission of the IFRS Foundation to develop Standards that bring transparency, accountability and efficiency to financial markets around the world.

What is scope of international accounting?

“International accounting extends general-purpose nationally oriented accounting in its broadest sense to (a) international comparative analysis, (b) accounting measurement and reporting issues unique to multinational enterprises, (C) accounting needs of international financial markets (d) harmonization of worldwide …

What is international finance and accounting?

International finance, sometimes known as international macroeconomics, is the study of monetary interactions between two or more countries, focusing on areas such as foreign direct investment and currency exchange rates.

What is the IASB due process?

The due process comprises the requirements followed by the International Accounting Standards Board when setting IFRS Standards and developing the IFRS Taxonomy, and by the IFRS Interpretations Committee when working with the Board to support consistent application of those Standards.

When did IASB assume its standard-setting responsibilities?

On April 1, 2001, the International Accounting Standards Board (IASB) assumed accounting standard-setting responsibilities from its predecessor body, the International Accounting Standards Committee.

What are the objectives of IASB Class 11?

Objectives of IASB: (i) To develop the single set of high quality global accounting standards so users of information can make good decisions and the information can be comparable globally. (ii) To promote the use of these high quality standards.

What is international harmonization of financial reporting?

On the simplest level, harmonisation is the process of bringing international accounting standards into some sort of agreement so that the financial statement from different countries are prepared according to a common set of principles of measurement and disclosure.

What roles do financial accounting standards play in the modern world?

The goal of financial accounting standards is to help stakeholders make informed investment decisions based on honest financial statements. The standards are designed to promote transparency in financial reporting. … This enables potential investors and creditors to make accurate evaluations of the businesses’ finances.

What is international accounting?

International accounting is a specialty within the entire discipline that is focused on using specific accounting standards that are as relevant in the US as they are when you are balancing the books of a company overseas. … Read on, and find out more about what global accounting is and why it is a popular choice.

What were the main reasons for the FASB to Favour rule based standards?

The FASB developed rules-based standards to increase verifiability for management, auditors and regulators who seek for a clear view of accounting issue. This is related to the reduction in litigation as guidance to protect them from any lawsuits or criticism for aggressive reporting (Benston et al., 2006).

How are accounting principles used in financial management?

The ultimate goal of any set of accounting principles is to ensure that a company’s financial statements are complete, consistent, and comparable. This makes it easier for investors to analyze and extract useful information from the company’s financial statements, including trend data over a period of time.