What is todays swap rate

Current29 Dec 20201 Year0.555%0.198%2 Year0.953%0.209%3 Year1.190%0.251%5 Year1.393%0.447%

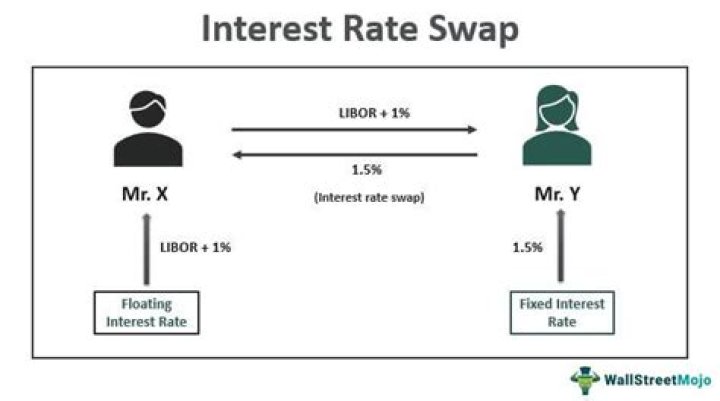

How does a LIBOR interest rate swap work?

Ultimately, an interest rate swap turns the interest on a variable rate loan into a fixed cost based upon an interest rate benchmark such as LIBOR (London Inter Bank Offered Rate), or the Secured Overnight Financing Rate (SOFR). … Then, the borrower makes an additional payment to the lender based on the swap rate.

What is today's LIBOR rate?

This weekMonth ago1 Month LIBOR Rate0.100.093 Month LIBOR Rate0.220.176 Month LIBOR Rate0.330.24Call Money2.002.00

What is LIBOR swap zero rate?

When principal amounts are added to both legs on the final payment date, the swap is rendered into an exchange of a fixed-rate bond for a floating-rate bond. … It follows that swap rates define par yield bonds and can be used to bootstrap the LIBOR zero curve (or LIBOIR/swap zero curve).What is 10 year LIBOR swap?

U.S. 10-year swaps measure the cost of swapping fixed rate cash flows for floating rate ones over a 10-year term. … Interest rate swaps are still referencing Libor, but in two years, it will SOFR (secured overnight financing rates), plus a fixed spread,” Belton said.

What currency swap means?

A currency swap is an agreement in which two parties exchange the principal amount of a loan and the interest in one currency for the principal and interest in another currency. At the inception of the swap, the equivalent principal amounts are exchanged at the spot rate.

What determines the swap rate?

The swap rate is the fixed rate of a swap. The cash flows are usually determined using the notional principal amount (a predetermined nominal value).

What is replacing GBP LIBOR?

By the end of 2021 GBP LIBOR will be replaced by SONIA (Sterling Overnight Index Average) as the Risk-Free Reference Rate for Sterling transactions. However it’s not as simple as just replacing one rate with another. To move to a different benchmark – in this case SONIA – there must be a market for that rate.What will banks use after LIBOR?

LIBOR is administered by the Intercontinental Exchange, which asks major global banks how much they would charge other banks for short-term loans. … LIBOR is being replaced by the Secured Overnight Financing Rate (SOFR) on June 30, 2023, with phase-out of its use beginning after 2021.

How is LIBOR calculated?Lenders use the following formula: principal x (Libor rate/100) x (actual number of days in interest period/360). According to USA Today, a typical adjustable rate mortgage (ARM) in the USA is based on a six-month Libor plus 2 to 3 percentage points.

Article first time published onWhat is the highest Libor rate ever?

Interbank Rate in the United States averaged 3.55 percent from 1986 until 2021, reaching an all time high of 10.63 percent in March of 1989 and a record low of 0.11 percent in September of 2021.

What is the swap rate for this 3 year swap?

TERM TO MATURITYClosing RateΔ MONTH3 Year1.230.135 Year1.590.1010 Year1.930.0115 Year2.08-0.03

How do you calculate swap duration?

- duration of swap=duration of long position−duration of short position.

- 0.125−0.75=−0.625,

- a negative duration. Effectively, when rates rise, his short position would be worth less. As a note of reference change in price=−duration⋅change in yield.

How is DV01 swap calculated?

estimate the change value given a change in the LIBOR swap curve. However, if the swap floating leg is 67% (or other percentage) of 1M/3M LIBOR, then DV01 = 67% X PV01.

Why do swap rates change?

Each day, information on swap rates across various maturities quoted by banks are collected and plotted on a graph, known as the swap curve. Due to the time value of money and the expectations of changes in the reference rate, different maturities will have different swap rates.

What are the benefits of currency swap?

It will reduce the costs of accessing foreign capital. Currency and interest rate swaps allow companies to navigate global markets more effectively. Currency and interest rate swaps bring together two parties that have an advantage in different markets.

What is swap value?

The value of a swap is its market value at any point in time. At inception, the value of an interest rate swap is zero. The price of the swap refers to the initial terms of the swap at the start of the swap’s life.

What are the two types of swaps?

- #1 Interest rate swap. Counterparties agree to exchange one stream of future interest payments for another, based on a predetermined notional principal amount. …

- #2 Currency swap. …

- #3 Commodity swap. …

- #4 Credit default swap.

What happens to arms when LIBOR goes away?

When the LIBOR disappears after the year 2021, your former LIBOR-based ARM will be attached to a new, like index. … Instead, a group called the Alternative Reference Rates Committee (which convened after the LIBOR scandal) may come up with a new benchmark rate based on repo trades backed by Treasury securities.

Will LIBOR really go away?

The statement highlights that global issuance of new LIBOR contracts will cease by December 31, 2021 and requirement of banks to reference new products to alternative reference rates.

Why will LIBOR be discontinued?

Why is LIBOR being phased out? After the 2008 Financial Crisis, interbank lending and borrowing began to decline as banks looked for other means to obtain financing. In addition, due to the inaccurate reporting of interest rates by some banks to ICE, LIBOR became vulnerable to rate manipulation and eroding credibility.

Is LIBOR ending in 2021?

On March 5, 2021, the applicable regulators announced that LIBOR will cease to be provided and will no longer be representative (i) immediately after December 31, 2021 for all sterling, euro, Swiss franc and Japanese yen settings, and the one-week and two-month U.S. dollar settings and (ii) immediately after June 30, …

What is happening to LIBOR in 2021?

LIBOR will cease for all currencies (other than USD) on 31 December 2021. The Financial Standards Board (FSB)1 and local regulators and working groups have recommended that market participants use robust alternative reference rates to LIBOR in new contracts wherever possible.

Why is the LIBOR rate so important?

LIBOR’s importance derives from its widespread use as a benchmark for many other interest rates at which business is actually carried out. also under investigation for misreporting LIBOr rates, with bank equity analysts estimating that fines and lawsuits could total almost $50 billion.

What was the highest mortgage rate in the 70s?

Thanks to Freddie Mac, there’s solid data available for 30-year fixed-rate mortgage rates beginning in 1971. Rates in 1971 were in the mid-7% range, and they moved up steadily until they were at 9.19% in 1974. They briefly dipped down into the mid- to high-8% range before climbing to 11.20% in 1979.

What was 2008 LIBOR?

1 Month LIBOR – Historical Annual Yield DataYearAverage YieldYear Low20082.68%0.44%20075.25%4.60%20065.10%4.40%

Is LIBOR higher than Sonia?

SONIA does not include a term bank credit risk component so is a better measure of the general level of interest rates than LIBOR. … Referencing alternatives such as SONIA is the most effective way of avoiding risks related to LIBOR discontinuation.

What is the 5 year mid swap rate?

5-Year Mid-Swap Rate Quotation means, in each case, the arithmetic mean of the bid and offered rates for the semi-annual fixed leg (calculated on the basis of a 360-day year of twelve 30-day months) of a fixed-for-floating U.S.

What is a 2 year swap rate?

2-Year Swap Rate (DISCONTINUED)-Market Yield on U.S. Treasury Securities at 2-Year Constant Maturity. … Rate paid by fixed-rate payer on an interest rate swap with maturity of two years. International Swaps and Derivatives Association (ISDA®) mid-market par swap rates.

What is 3m Libor?

3-month LIBOR Rate means the rate for deposits in U.S. … Dollars having a term of three months, as published on the first Business Day of each week during the relevant Calendar Period immediately preceding the Distribution Period for which the Floating Rate is being determined.

How are swaps calculated?

Swap = (Pip Value * Swap Rate * Number of Nights) / 10 Note: FxPro calculates swap once for each day of the week that a position is rolled over, while on Friday night swap is charged 3 times to account for the weekend.