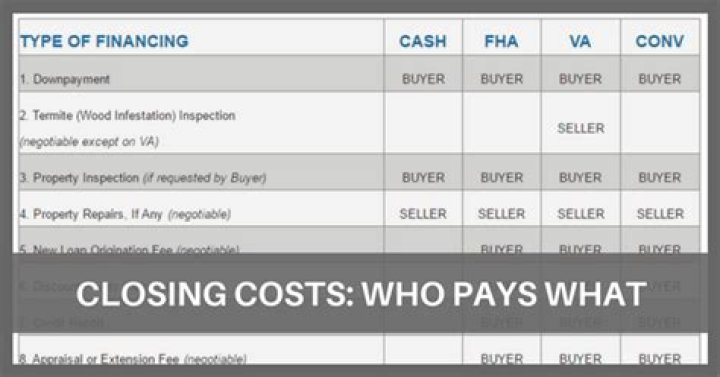

Who pays FHA closing costs

Ask the seller to pay closing costs FHA rules allow the seller or another third party to pay up to 6% of the property sales price toward closing costs or other prepaid expenses.

What does the seller pay on an FHA loan?

For all FHA loans, the seller and other interested parties can contribute up to 6% of the sales price or toward closing costs, prepaid expenses, discount points, and other financing concessions. If the appraised home value is less than the purchase price, the seller may still contribute 6% of the value.

How much should closing costs be on a FHA loan?

FHA closing costs average anywhere from 2% to 4% of the loan amount. Your actual costs will be tied to various factors such as your loan amount, credit score, and lender fees. Some of the costs are standard for all FHA loans, while others are lender-based or third party costs such as your appraisal.

Why are FHA loans bad for sellers?

Unfortunately, some home sellers see the FHA loan as a riskier loan than a conventional loan because of its requirements. The loan’s more lenient financial requirements may create a negative perception of the borrower. And, on the other hand, the stringent appraisal requirements of the loan may make the seller nervous.How can I avoid paying closing costs?

- Look for a loyalty program. Some banks offer help with their closing costs for buyers if they use the bank to finance their purchase. …

- Close at the end the month. …

- Get the seller to pay. …

- Wrap the closing costs into the loan. …

- Join the army. …

- Join a union. …

- Apply for an FHA loan.

Can closing costs be rolled into FHA loan?

FHA guidelines do permit some of the closing costs to be rolled into the loan. They are clear that the down payment amount of 3.5% required to close the loan may not be financed and must be paid for independently.

Can the seller pay the down payment on FHA loan?

Seller Cannot Pay Borrower’s Down Payment (“MRI”) on FHA Loans. … That’s the minimum down payment required for this particular program. Home buyers who want to use an FHA-insured mortgage loan to buy a house generally must put down at least 3.5% of the property’s value.

What will fail an FHA inspection?

Structure: The overall structure of the property must be in good enough condition to keep its occupants safe. This means severe structural damage, leakage, dampness, decay or termite damage can cause the property to fail inspection. In such a case, repairs must be made in order for the FHA loan to move forward.How long do I have to wait to sell my FHA home?

How long before you can sell your home purchased with an FHA mortgage? The answer is really, whenever you have the need. But depending on circumstances you may find your ability to sell is more limited in the first 90 days of ownership.

How long does it take to close a FHA loan?It takes around 47 days to close on an FHA mortgage loan. FHA refinances are faster and take around 32 days to close on average. FHA loans generally close in a very similar timeframe to conventional loans but may require additional time at specific points in the process.

Article first time published onDoes credit score affect closing costs?

One of the main factors in the amount of closing costs you’ll pay is your credit score, the lower your score, the more risky the loan is, the higher your closing costs will be. If you have a good credit score, you can go to any bank and get a loan.

Is my down payment included in closing costs?

Do Closing Costs Include a Down Payment? No, your closings costs won’t include a down payment. But some lenders will combine all of the funds required at closing and call it “cash due at closing” which bundles closing costs and the down payment amount — not including the earnest money.

Why would a seller pay closing costs?

By having the seller pay for certain items in your closing costs, it enables you to make a higher offer. Therefore, you’ll effectively be paying your closing costs throughout the life of the loan rather than upfront at the closing table because they’re now built into your loan amount.

Can you negotiate seller to pay closing costs?

The short answer is yes – when you’re buying a home, you may be able to negotiate closing costs with the seller and have them cover a portion of these fees.

Can I roll closing costs into my mortgage?

In simple terms, yes – you can roll closing costs into your mortgage, but not all lenders allow you to and the rules can vary depending on the type of mortgage you’re getting. If you choose to roll your closing costs into your mortgage, you’ll have to pay interest on those costs over the life of your loan.

What is the 373 rule?

MDIA. Timing Requirements – The “3/7/3 Rule” The initial Truth in Lending Statement must be delivered to the consumer within 3 business days of the receipt of the loan application by the lender. The TILA statement is presumed to be delivered to the consumer 3 business days after it is mailed.

Do FHA loans hurt your credit?

If you want to buy a home with an FHA mortgage, or refinance an existing home loan with an FHA refinance loan, you don’t have to use your current lender. Some borrowers worry that doing this with multiple lenders will negatively affect their credit score. …

Do you have to pay closing costs up front?

The upside of writing a check for your closing costs when you finalize your mortgage is that you don’t have to take on more debt when you buy a home. If you roll your closing costs into your loan, you pay interest on them. Pay them up front, and you don’t, which keeps your monthly payment lower.

Is it better to go conventional or FHA?

FHA might be better than conventional if you have a credit score below 680, or higher levels of debt (up to 50% DTI). Conventional loans become more attractive the higher your credit score is, because you can get a lower interest rate and monthly payment.

Can I sell my FHA home and get another FHA loan?

FHA allows you to only have one loan at any given time. Therefore, if you plan to sell one home and buy another, you may do so as long as you are paying off the existing FHA loan in order to purchase your new home with yet another FHA loan.

Can I get an FHA loan if I already own a home?

Since the FHA loan requirements are relaxed, most people find that it’s a great way to buy their first home, but it can be used on any home — even a second home if you already own one.

Can an FHA loan close in 30 days?

You can typically close on an FHA purchase or refinance within 30 days of submitting your loan application.

Why would an underwriter deny an FHA loan?

There are three popular reasons you have been denied for an FHA loan–bad credit, high debt-to-income ratio, and overall insufficient money to cover the down payment and closing costs.

Is there a penalty for paying off an FHA loan early?

FHA loans, which are federally backed mortgages designed for low- and moderate-income borrowers, do not have any prepayment penalties.

How do I include closing costs in my loan?

- Pay all closing costs out of pocket on closing day.

- Negotiate seller concessions where the seller pays for some or all of the costs.

- “Buy up” the interest rate so that the lender pays for some or all of the costs (known as ‘lender credits’)

Which fee is not allowed to be charged to the borrower in an FHA loan?

FHA offers a reverse mortgage known as the Home Equity Conversion Mortgage (HECM). Borrowers are prohibited from paying more than $6,000 for a HECM lender’s origination fee and lenders may not charge more than this total amount on any loan, according to Mortgagee Letter 08-34.

What kind of interest rate can I get with a 780 credit score?

Fixed-rate loans ensure your interest rate stays the same over the entire term of your loan, despite outside market factors. An “excellent” credit score of 780 would have earned you a 3.87 percent rate in October, NerdWallet reported then. (Rates have risen and are higher now.)

What is due at closing?

Here’s the gist: Closing costs consist of a variety of charges for services and expenses required to complete your mortgage. These costs may include property fees (appraisals and inspections), loan fees (for applications, attorneys, and origination), insurance fees, title fees, property taxes, and even postage fees.

What are 4 C's of underwriting?

“The 4 C’s of Underwriting”- Credit, Capacity, Collateral and Capital.

Who pays title fees at closing?

Closing costs are paid according to the terms of the purchase contract made between the buyer and seller. Usually the buyer pays for most of the closing costs, but there are instances when the seller may have to pay some fees at closing too.

Does the seller pay closing costs out of pocket?

Your closing costs, as a seller, will be deducted from proceeds you make on the home, unless you have low equity, in which case you may need to cover some expenses out of pocket. The amount of money you walk away with after these costs is referred to as your net proceeds.