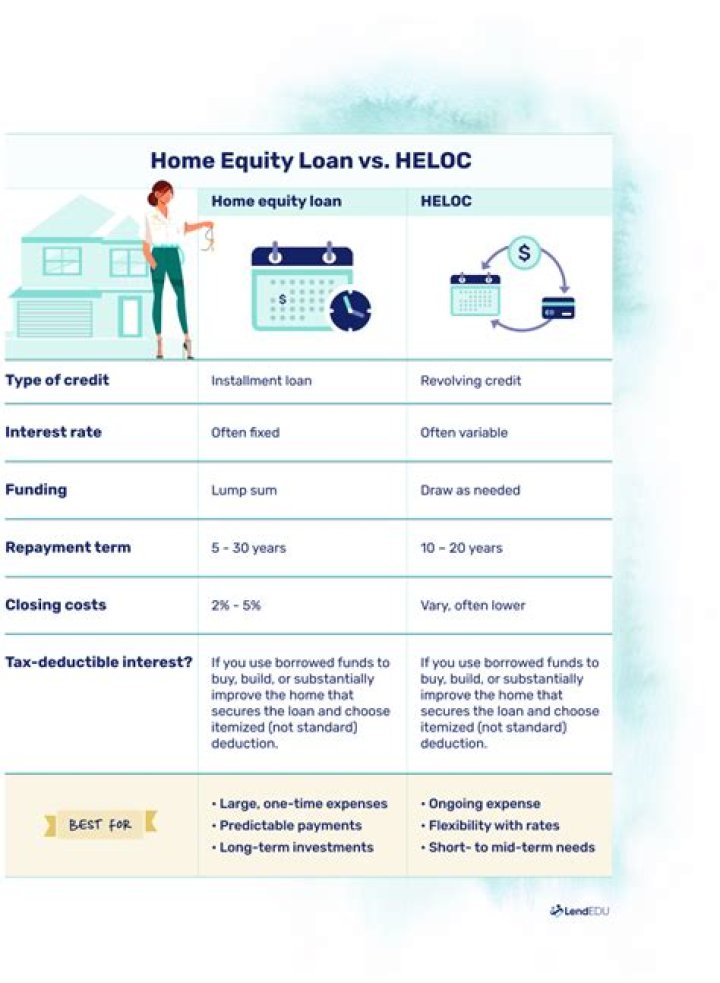

What is a fixed equity loan

Home equity loans typically carry fixed interest rates that are often lower than credit cards or other unsecured consumer loans. In a changing rate environment, a fixed rate loan can provide simplicity in budgeting, because your monthly payment amount remains the same over the life of the loan and will never increase.

What is the benefit of a fixed rate home equity loan?

Home equity loans typically carry fixed interest rates that are often lower than credit cards or other unsecured consumer loans. In a changing rate environment, a fixed rate loan can provide simplicity in budgeting, because your monthly payment amount remains the same over the life of the loan and will never increase.

What is an equity loan and how does it work?

A home equity loan, also known as a second mortgage, enables you as a homeowner to borrow money by leveraging the equity in your home. The loan amount is dispersed in one lump sum and paid back in monthly installments.

What is fixed first equity loan?

Fixed rate loans provide a single lump-sum payment to the individual. The amount can be repaid over a set period at the agreed upon interest rate. The interest rate does not fluctuate depending on market conditions and remains the same over the lifetime of the loan.What is a fixed home equity?

A home equity loan’s interest rate is fixed, meaning the rate doesn’t change over the years. Also, the payments are fixed, equal amounts over the life of the loan. A portion of each payment goes to interest and the principal amount of the loan.

Can you borrow money any time with a home equity loan?

You don’t receive a lump sum with a home equity line of credit (HELOC) but rather a maximum amount available for you to borrow—the line of credit—that you can borrow from whenever you like. You can take however much you need from that amount.

How much equity can you borrow from your house?

Depending on your financial history, lenders generally want to see an LTV of 80% or less, which means your home equity is 20% or more. In most cases, you can borrow up to 80% of your home’s value in total. So you may need more than 20% equity to take advantage of a home equity loan.

How much equity do you need to buy a second house?

Equity is the difference between your property value and the amount you have owing on your home loan. To qualify: You can generally release up to 80-90% of the value in your property in equity to buy a second property. You must owe less than 80% of the property value on your home loan.Is a fixed home equity loan closed end?

Closed-end (fixed) home equity loans are closed-end loans secured by the member’s dwelling. These types of loans are often referred to as second mortgage loans, even though they may not be in second lien position. … The Loan Estimate must be in writing and only contain the information prescribed in 1026.37.

How long does an equity loan take?The truth is that home equity loan approval can take anywhere from a week—or two up to months in some cases. Most lenders will tell you that the average window of time it takes to get a home equity loan is between two and six weeks, with most closings happening within a month.

Article first time published onDo you have to pay back equity?

When you get a home equity loan, your lender will pay out a single lump sum. Once you’ve received your loan, you start repaying it right away at a fixed interest rate. That means you’ll pay a set amount every month for the term of the loan, whether it’s five years or 15 years.

How do I pay back my equity loan?

You don’t have to pay off the whole equity loan in one go. But the rules state you have to repay at least 10% of the property’s current value. For example, you could repay 10% of the property’s current value if you took out a 20% loan, or repay 10%, 20% or 30% of the property’s current value if you borrowed 40%.

Does a home equity loan require an appraisal?

In a word, yes. The lender requires an appraisal for home equity loans—no matter the type—to protect itself from the risk of default. If a borrower can’t make his monthly payment over the long-term, the lender wants to know it can recoup the cost of the loan. An accurate appraisal protects you—the borrower—too.

Is there a penalty for paying off a home equity loan early?

Home equity loans don’t usually have prepayment penalties, so you don’t need to worry about paying extra money if you want to pay your loan off early.

What are the disadvantages of a home equity line of credit?

- HELOCs can come with a minimum withdrawal amount.

- There can be limitations to how you access the funds.

- There is a set withdraw period after which you cannot access any further funds.

- There can be fees associated with a HELOC.

- You can hurt your credit if you do not make payments on time.

- Harder to qualify right now.

What does it mean to borrow against your house?

Home equity loans allow homeowners to borrow against the equity in their residence. Home equity loan amounts are based on the difference between a home’s current market value and the mortgage balance due. Home equity loans come in two varieties—fixed-rate loans and home equity lines of credit (HELOCs).

What is the monthly payment on a $100 000 home equity loan?

Assuming principal and interest only, the monthly payment on a $100,000 loan with an APR of 3% would come out to $421.60 on a 30-year term and $690.58 on a 15-year one. Credible is here to help with your pre-approval.

What is the monthly payment on a $200 000 home equity loan?

On a $200,000, 30-year mortgage with a 4% fixed interest rate, your monthly payment would come out to $954.83 — not including taxes or insurance.

What is the payment on a 50000 home equity loan?

Loan payment example: on a $50,000 loan for 120 months at 3.80% interest rate, monthly payments would be $501.49.

What do most homeowners use equity for?

Homeowners sometimes use home equity to pay off other personal debts, such as car loans or credit cards. “This is another very popular use of home equity, as one is often able to consolidate debt at a much lower rate over a longer-term and reduce their monthly expenses significantly,” Hackett says.

How can I get the equity out of my home without selling it?

Home equity loans, home equity lines of credit (HELOCs), and cash-out refinancing are the main ways to unlock home equity. Tapping your equity allows you to access needed funds without having to sell your home or take out a higher-interest personal loan.

What can I do with equity?

You can tap into this equity when you sell your current home and move up to a larger, more expensive one. You can also use that equity to pay for major home improvements, help consolidate other debts or plan for your retirement. Not all homeowners have equity in their homes.

What is a blanket mortgage in real estate?

A blanket mortgage, often called a blanket loan, is a type of mortgage that finances multiple real estate properties at the same time. Popular among real estate investors, developers and owners of commercial property, blanket loans can make the lending process more efficient and cost effective.

What creates a closed mortgage?

A closed-end mortgage (also known as a “closed mortgage”) is a restrictive type of mortgage that cannot be prepaid, renegotiated, or refinanced without paying breakage costs or other penalties to the lender. … Closed-end mortgages also prohibit pledging collateral that has already been pledged to another party.

How do I get out of a closed mortgage?

Renegotiate to take advantage of a better rate or to pay off your mortgage faster. Refinance to lower payments, consolidate debt, or add a Home Equity Line of Credit for renovations or investing purposes. Switch to a different lender for better rates or terms. Pay out your mortgage entirely.

Can you use equity on a fixed loan?

Yes, you can, but you’ll be hit with LMI fees. If your home loan is over 80% of the value of your property or 80% LVR, mortgage insurance kicks in, a one-off fee that most banks charge to mitigate their risk.

Can I use my house as collateral to buy another house?

Only the home being purchased can be used as collateral. When it comes to buying real estate, the home you purchase is always the collateral for that loan. Most banks will not allow you to use one home as collateral when buying another home.

Can you use equity as a down payment?

Can You Use a Home Equity Loan to Make a Down Payment on a Home? Yes, if you have enough equity in your current home, you can use the money from a home equity loan to make a down payment on another home—or even buy another home outright without a mortgage.

How do you pull equity out of your house?

- Pay off your mortgage. The single most effective way to increase your home equity is to pay off your mortgage faster than anticipated. …

- Increase the value of your home. …

- Refinance to a shorter loan. …

- Improve your credit score. …

- Take advantage of market fluctuations.

How long does it take to build equity in your home?

Because so much of your monthly payments go to interest at the beginning of the loan term, it often takes about five to seven years to really begin paying down principal. Plus, it usually takes four to five years for your home to increase in value enough to make it worth selling.

Are there closing costs on a HELOC?

HELOC closing costs Closing costs for a HELOC are often a bit lower than the costs of closing a primary mortgage, but the average closing costs for a home equity loan or line of credit (depending on the lender and the loan product) can add up to between 2 percent and 5 percent of your total loan cost.